- California Financial Advisor Wins FINRA Expungement of False Unsuitability Claim

- RIA Compliance Blind Spot: The Risk Of A Generic IAR Agreement

- Texas Financial Advisor Wins FINRA Expungement of False Solicitation Allegation

- SEC Regulation S-P Modernization: June 2026 RIA Deadline Guide

- Modernizing FINRA Arbitration: The Looming Threat to Form U5 Expungement

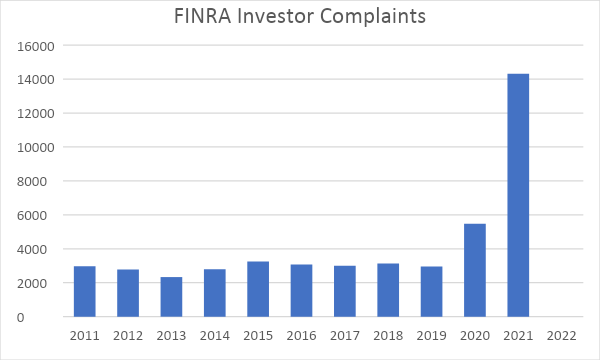

Seeing the entire picture often requires that we take a step back. Below is a chart showing the number of customer complaints against financial advisors received by FINRA, per year, since 2011.

FINRA will release 2022 data early next year, but we can be sure that the precipitous fall of the market indexes is directly correlated to the number of investor complaints.

So what can you do to safeguard yourself against this tsunami?

If you currently have NO BrokerCheck disclosures, and you receive a new customer complaint, you should consider talking to an attorney outside of your firm. The reason is two-fold:

First, your firm will likely tell you that they’ll “handle it all for you,” but that’s only partially true. They will handle the logistics of settling the complaint, but at the end of the day, those attorneys represent the firm and not you. That conflict of interest is typically not addressed ahead of time, and it’s you who will receive the complaint disclosure on your record — whether or not you financially contribute to that settlement.

Second, FINRA will likely send you an inquiry letter regarding the alleged sales-practice violation. Upon receipt of that inquiry letter, you must defend against both the investor complaint and the FINRA investigation. Again, it won’t be in your best interests that are prioritized by your in-house counsel — they will make sure that any information provided to FINRA shows no fault on the part of the firm. To make matters worse, that information may or may not be congruent with the information that you need to send to FINRA in your own defense.

The safest bet is to simply hire your own counsel.

If you DO currently have BrokerCheck disclosures, you should still do everything listed above, for starters.

Because you already have disclosures on your record, you may inadvertently be a larger target for new customer complaints — without even knowing it. Our research shows that your chance of getting a brand-new customer complaint is roughly five times higher when your BrokerCheck profile already contains a disclosure. Why? Because BrokerCheck houses the data that investor attorneys harvest to find who they should target next. Any pattern of complaints, along with past settlements, demonstrates an optimal situation to gain a “nuisance” settlement.

So in addition to hiring your own counsel, it’s highly advised to seek expungement of your disclosures. Not every disclosure can be removed, but most customer complaints, U5 termination allegations, criminal disclosures, and tax liens have a viable route for expungement.

And you should hurry. FINRA has a rule proposal with the SEC that should be decided upon soon and would tighten down many portions of the expungement process.

Firms and advisors alike should be paying attention to the disturbing trend among investors to lodge claims against their advisors when the markets are down. As of the writing of this post, the S&P 500 index is down nearly 25% from its highs, YTD, and 2022 to 2023 (given the complaint lag) may be one of the most frenzied periods in recent memory.